The Trillion-Dollar Debate: Carried Interest, Tax Loopholes, and What Voters Don’t Know

Why fund managers pay a lower tax rate than you

The News

In every election cycle, one (or both) candidates often promise to finally close what’s known as the carried interest tax “loophole.” This tax policy has reportedly saved fund managers over $1 trillion since 2000. However, the issue typically fades from the spotlight as campaigns progress. A cynical explanation might be that the financial industry’s powerful lobbying efforts effectively shut down any proposed changes that could harm their interests. But I believe the real reason is that most voters don’t actually understand what carried interest is or how it works, so it falls to the bottom of the priority list in campaign messaging.

To grasp the nuances of this tax policy, it’s important to first understand how fund managers make money. This includes hedge fund managers, private equity investors, and venture capitalists. For the purpose of this article, we’ll focus on venture capital, since many people have at least a basic understanding of what they do — invest in startups.

The Concept

A venture capital (VC) firm raises money from outside investors known as Limited Partners (LPs), which often include wealthy individuals, pension funds, endowments, and family offices that manage the wealth of affluent families. The VC firm, known as the General Partner (GP), then uses this capital to invest in startups with the goal of helping them grow and eventually be sold or go public, thereby generating returns for the investors.

The VC firm organizes the capital it raises into distinct funds. For example, it might raise a “Fund 1” of $50 million, and a few years later, raise a “Fund 2” of $100 million. The GP has a set period to invest the capital from these funds into promising startups. When these startups grow, get acquired, or go public (IPO), the fund ideally generates a return greater than the initial investment, and the profits are then distributed back to the LPs.

VC firms generate income in two primary ways. The first is through management fees. VC firms charge their LPs an annual fee, typically around 2% of the total fund size, to cover the costs of managing their investments. These costs include salaries, rent, travel, and research. For instance, if your VC firm raised a $100 million fund, you would charge 2% of that amount ($2 million) annually as a management fee. This fee is paid whether or not the investments are successful.

The second—and more lucrative—way VC firms make money is through carried interest. This represents the firm’s share of the profits after returning the initial capital to the LPs. Typically, carried interest is around 20% of the profits. You can think of this as a performance-based bonus or commission, rewarded for delivering strong returns on the investments.

The Example

Let’s say your VC firm launched a fund and invested $10 million across five startups, acquiring a 20% ownership stake in each. A few years later, four of the startups fail, but one is sold to Google for $1 billion. With a 20% stake, the VC firm would receive $200 million from the sale. Of that $200 million, the first $10 million would be returned to the LPs as their initial investment, and the remaining $190 million profit would be split between the VC firm and the LPs. The VC firm would typically take 20% of the profit ($38 million) as carried interest, while the LPs would receive the remaining 80% ($152 million).

Now, let’s discuss how these VC investors are taxed. The individuals at the firm earn money in two main ways. First, they receive salaries and bonuses, similar to employees at any other company, which are paid through the management fees. These earnings are taxed at the standard income tax rate, which can be as high as 37% federally. In addition, the partners of the firm share the carried interest, which is taxed at the lower capital gains rate, capped at 20% federally.

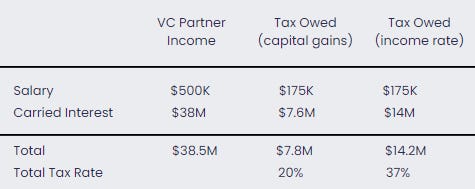

To illustrate the tax implications, let’s compare the taxes owed by a VC partner if the carried interest were treated as capital gains versus earned income, assuming the VC firm has only one partner. You can see from the chart below that there would be a substantial difference if this policy was changed.

The Quiz

In place of today’s quiz, I’d love to hear your thoughts on reasons for or against changing this policy. Post in the comments below or just reply to this email. There are great arguments on both sides!

Relevant Course

Most (not all) of my articles will incorporate concepts and frameworks covered in our courses at Pareto Labs. If you want to learn more about capital gains vs. earned income and how it applies to employee and founder stock options and equity grants, check out our course. Tommy and I cover it with a 1990s infomercial theme to keep you entertained!

Thanks for the great explanation

In a world with an ever increasing wealth gap I think it's unfair and unhelpful that unearned income is given such a huge tax break compared to earned income. Closing the carried interest loophole would be a great, small step in my opinion. Let the LPs keep their long term gains treatment - if the GPs want it too then they should invest as an LP too.

That's not even considering the sticky part where carried interest is a performance fee. And what's a performance fee if not earned - as in earned income.